Localism is the proactive administrative, economic and societal empowerment of places and their people. Across the world it is a force that battles against the natural centralist instincts of national governments.

Localism is the proactive administrative, economic and societal empowerment of places and their people. Across the world it is a force that battles against the natural centralist instincts of national governments.

Some societies are comfortable with federal structures that allow degrees of local independence. Others, more centrally directed, are far less tolerant of local deviation. At this time the UK is rapidly discovering that greater localism is a key to future international prosperity.

This shift towards stronger, more-empowered, local leadership has many champions across the political spectrum – and they are supported by many public and private actors.

Opposing these champions are the massed ranks of established national forces and major utilities. They worry that fragmentation leads to a loss of control, a slide towards fiscal indiscipline and greater complexity. Trust and experience in a common cultural adherence are key issues – defining a sense of identity.

But, while the shift has been debated for years as an issue in domestic politics, it is international trade that drives the more recent place-making emphasis. Localism is a global issue.

At this time when the UK national government is entangled in disentanglement from the European Union, central policy developers (with their dependence on macro-economic approximations) are painfully aware that their science is largely based on the aggregation of many local economic communities each with diverse needs and priorities.

Onto this stage now enter the long-promised metro-mayors and cities emboldened by new concerns for life after Brexit. Add in some fracturing of old political orders and the scene is set for a considered reordering of governmental structure – or possibly opportunistic power plays.

At its best Localism is about people and places. The people comprise residents, visitors and commuting employees. Businesses may create jobs, pay local property taxes and have expectations of local infrastructures but their employees, often commuting from far and wide, have no local democratic voice where they work. Heavily dependent on the redistribution of national taxation, Local Authorities are reduced to insignificant branch agencies with occasional competitive battles to adjust some funding formula that rarely reflects local priorities. Some places are sufficiently enlightened to spend public money predominantly with local suppliers – thus investing in greater local money circulation before it is syphoned away to big brands and Treasury coffers.

Local levers of power are minimal and this frustrates local leaders whose citizens expect them to promote local economic and social well-being. Woe betide, however, those places that fall markedly below common (nation-wide) expectations and risk outraged complaints of ‘Post-Code Lotteries’ and Daily Mail headlines.

Yet we know that some places are more successful that others. Some places seem to attract inward investment in ways that others do not. Some seem able to retain and employ their young people whilst others see only a drift away from home. Some places have a track record in creating new types of employment but others never recover from the demise of old industries. Some seem destined to be losers and never manage to catch the funding streams.

But we also know why some fail where others do not. Some attribute the differences to location, weather, historical accidents, insensitive policies or outmoded formulaic funding rules. Some places have been over dependent on outmoded industries and have not seen far enough ahead to plan a different future. But, most of all, the performance variations come down to the quality of locally collaborative leadership.

This much was recognised by Lord Heseltine’s Local Enterprise Partnerships – bodies that were, alas, quickly dominated by big-brand placemen – public or private. Fostering collaborative and constructive local leadership takes years – way longer than electoral cycles. And it demands a real understanding of local ecosystems.

All that was known and understood way before creation of the European Union. Pre-dating that by several hundred years, cities across northern Europe created the Hanseatic League – a trusted trading network that enabled deep relationships, economic wellbeing and cultural confidence.

The Hanseatic League still has echoes in modern times; embedded in an airline name and in the Business Hanse – an active network of enterprises seeking deeper cross border trade. UK cities, mostly facing the North Sea, very clearly understood that confident trading needed much more than a simple market – it demanded trust and whole community support. And building on those formative experiences the ‘new’ place-based strategists can understand why some communities succeed where other decline.

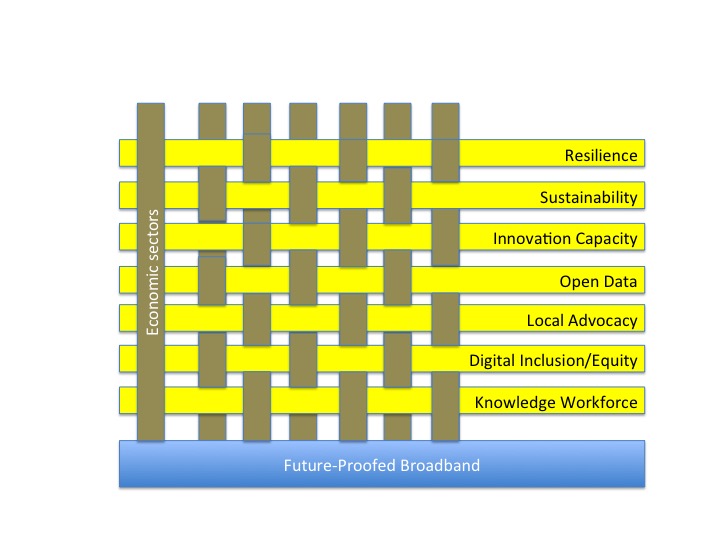

This is is why, instead of just puzzling over raw economic data and demographics, successful communities are now being assessed on the deeper quality of local programmes that cut across the top-down sector silos. Creating and sustaining a range of these initiatives requires long-term dedication and a spirit of willing community collaboration – from schools to hospitals, from transport providers to colleges and universities and, vitally, full engagement with really local small business ventures. Hence the recent calls for greater recognition of local business/community responsibilities.

This is is why, instead of just puzzling over raw economic data and demographics, successful communities are now being assessed on the deeper quality of local programmes that cut across the top-down sector silos. Creating and sustaining a range of these initiatives requires long-term dedication and a spirit of willing community collaboration – from schools to hospitals, from transport providers to colleges and universities and, vitally, full engagement with really local small business ventures. Hence the recent calls for greater recognition of local business/community responsibilities.

All that, of course, would be helped by a central government that saw its role as an enabler, nurturing local differentiation, instead of a state supervisor determined to scold any local experiment that falls a little short of the lowest common denominators of cost-constrained public services.

All this we know from the evidence of hundreds of places around the world that have defied expectations and breathed new life into their communities. Building on capabilities that leverage the Smart’ technological enthusiasms of major cities, we are now seeing recognition of a newly empowered breed of ‘Intelligent Communities’. Some achieve this because, simply, “we’ve had enough” and others through inspired local leadership – but, crucially, all are making a name for themselves on the global stage.

It’s a puzzle for sure when we have an abundance of ‘fairly average’ national economic data but very little local data granularity to enlighten aspiring city leaders.

So when the central ‘industrial strategists’ scratch their heads and our political classes try to imagine how to recover from natural disasters or self-inflicted wounds, this time, we’d hope, the old sectorial orders must be refashioned – supplemented and overlaid with place-based and inclusive, locally-led, economic and societal nutrients. Tolerance and flexibility for their encouragement from the top down will (or should) seek accommodation with local homegrown energies.

______

This article was written as a discussion paper for the Global Summit Steering Group 2018.

Tags: broadband, digital, innovation, Municipal Enterprise, policy, sustainability